On December 19th, county officials presented Commissioners with a crash course in property taxes. Erica Strickland, Park County Finance Director, discussed the process for calculating property taxes, the key players involved, the reasons behind the increase in taxes, and what the change means for the county budget. Here are the takeaways:

How are property taxes calculated?

Every 2 years, the Department of Revenue conducts a statewide assessment of the market value of property. The market values seen on the 2023 tax bill are based on assessments performed in January 2022. According to the Montana Code Annotated (MCA), market value is “the value at which property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or sell and both having reasonable knowledge of relevant facts.” The taxable value of a property is determined by multiplying the assessed market value of a property by the assigned tax rate. The residential property tax rate is 1.35%. The agricultural rate is 2.16%. The commercial rate is 1.89%.

Assessed Market Value X Tax Rate = Taxable Value

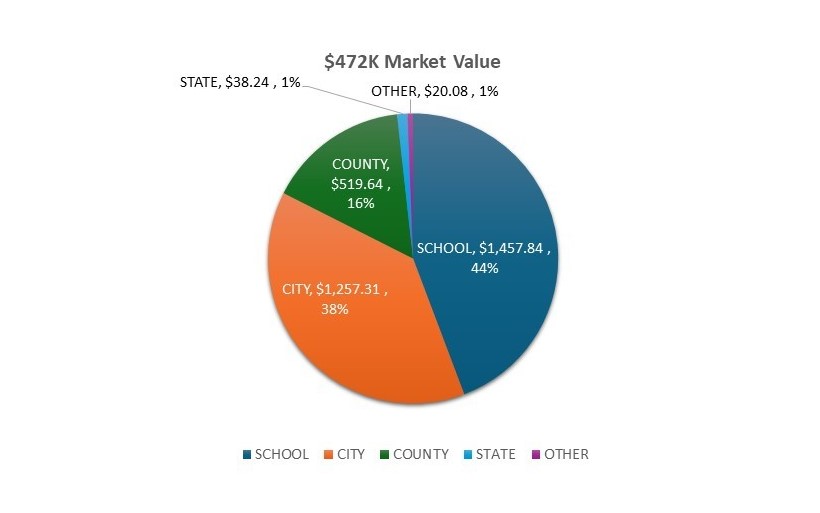

Livingston Residential Property Example

$472,000 (Market Value) X 1.35% (Residential Tax Rate) = $6,372 (Taxable Value)

Property taxes are highly individualized. The dollar amount you contribute to a specific tax component is determined by a combination of levies and assessments. Property type, location within the county, and whether the property is within city or town limits are factors that influence which levies appear on your tax bill. A tax bill contains levies for schools, the county, the state, and applicable municipality (City of Livingston or Town of Clyde Park). Levies are applied against taxable values. Assessments are flat fees assigned for a service. The county only refuse fee is an example of an assessment.

Livingston Residential Property Tax Breakdown

There are 3 types of Park County Levies: floating, voted, and permissive.

|

Floating

|

Voted

|

Permissive

|

|

Floating levy increases are limited to half the rate of 3 years inflation, or 2.46 percent in 2023, plus new construction which totaled about 5 percent.

|

Voted levies are approved by voters and can be either a fixed number of mills or a fixed dollar amount. Ballot language defines the number of mills or fixed annual dollars to raise, the term of the levy, and the defined use of funds.

|

Permissive levies are set by the MCA to defray costs to budget.

|

|

Examples of county-wide floating levies include the general mill (funds multiple departments), search & rescue, and Angel Line.

Roads, ambulance (county only portion), and planning are examples of county only floating levies.

|

The ambulance, library, and Angel Line are supported by voted levies in addition to the floating levies.

For example, the ambulance receives $185,891 annually through a fixed dollar voted levy and 8.86 mills (with a 10-year sunset) through its fixed mill voted levy.

|

The Medical Levy and the Sheriff’s Retirement Levy are examples of permissive levies.

The permissive medical levy allows the county to levy employee health insurance rates exceeding the rate paid per employee for full coverage in the year 2000.

The permissive Sheriff's Retirement Levy allows the county to levy 3% of Sheriff’s Office Retirement Employer Contributions to account for increase in rates around 2017.

|

Gardiner Residential Property Example

$600,000 (Market Value) X 1.35% (Residential Tax Rate) = $8,100 (Taxable Value)

Taxable Value X Number of Mills / 1000 = Levied Taxes

$8,100 (Taxable Value) X 291.05 (Number of Mills) / 1000 = $2,357.05 (Levied Taxes)

Levied Taxes + Assessments = Tax Billed

$2,357.05 (Levied Taxes) + $227 (Refuse Assessment) + $7 (Soil & Water Assessment) = $2,591.05 (Tax Billed)

Who is involved?

The Legislature determines tax rates and exemptions. The legislature assigns a tax rate to each of the 16 property tax classes. Tax rates range from .29% to 15.12%. The most common tax rates are residential, commercial, agricultural, and forest.

The state levies 95 school equalization mills, up from 77.9 mills last year, and 6 university mills. School equalization mills are collected by each county and distributed by the state to school districts. The purpose of the equalization mills is to equalize funding between richer and poorer school districts across the state.

The Department of Revenue’s Property Assessment Division provides the classification and valuation for properties. The Property Assessment Division then determines a property’s taxable value by multiplying the market value by the tax rate.

The Department of Revenue provides the county with the total taxable value of property located within each jurisdiction within a county. The total taxable value of property in Park County is $91,664,988, up 37% from last year. The value of a mill in Park County is $91,665. The county uses the total taxable value to determine how many mills are needed for the budget.

The Park County Treasurer sends the tax bill and collects taxes.

A 37% increase in taxable value does not equal a 37% increase in county revenue.

Even though the taxable value goes up 37%, the county revenue does not increase by 37%. County revenue is restricted by floating levies. The county budget supported by floating levies can grow at half the rate of inflation over a 3-year period, or 2.46% in 2023, plus any taxable value from new construction. There is an inverse relationship between floating levies and taxable value. When taxable values go up, floating levies go down. Voted levies do not have the same restriction because they have been approved by voters. When taxable values increase, voted and permissive levies get a larger share of the revenue pot. For example, the library and ambulance, which has both floating and voted levies, increased revenue by 22% and 29%, respectively.

School, City, and State levies can increase your overall tax bill, irrespective of the county tax structure. The County does not directly handle school or city budgets. It is also noteworthy that residential taxable values are increasing faster than commercial and agricultural taxable values, placing an increased tax burden on residential properties. If residential market values significantly decreased, the tax burden on commercial and agricultural properties would increase.

Where can I find more information?

To learn more about property taxes:

- View the Department of Revenue’s Property Appraisal Town Hall at https://mtrevenue.gov/property/

- Review Park County Finance Director Erica Strickland’s presentation on property taxes at https://parkcounty.granicus.com//ViewPublisher.php?view_id=1

To view your property tax bill:

- Park County Treasurer: https://www.parkcounty.org/Government-Departments/Treasurer/

To view your property assessment:

- https://svc.mt.gov/dor/property

If you believe the description of your property is incorrect, contact the Department of Revenue directly:

- https://mtrevenue.gov/contact/field-office-locations/#Contact-Information-By-County-919